Nada A.

Before 365:

Software Tester | Testing Geeks

After 365:

Senior Data Engineer | VOIS

See all reviews

Master time series forecasting in Python: Gain solid theoretical knowledge and work with popular time series models such as ARIMA, ARCH, and GARCH

Skill level:

Duration:

CPE credits:

Accredited

Bringing real-world expertise from leading global companies

Bachelor's degree, Mathematics & Economics

Description

Curriculum

Free lessons

1.1 What does the Course Cover

4 min

2.1 Setting up the Environment

1 min

2.2 Installing the Necessary Packages

1 min

3.1 Introduction to Time Series Data

4 min

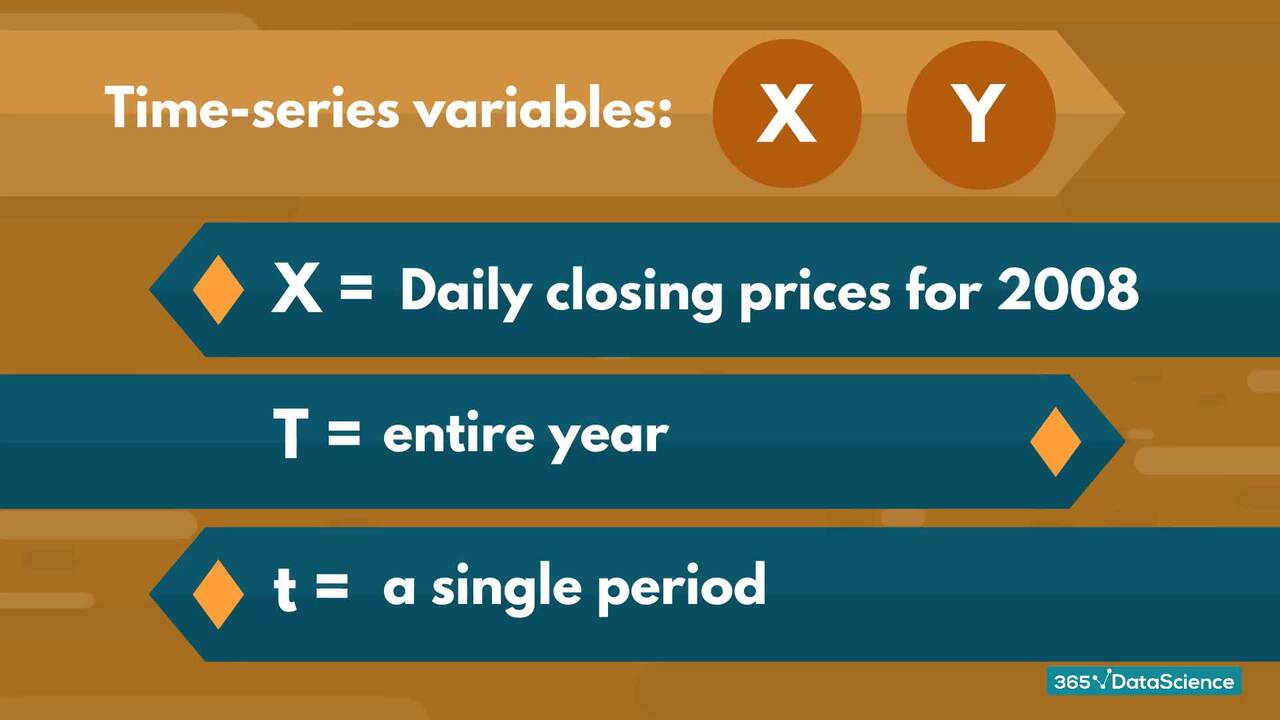

3.2 Notation for Time Series Data

1 min

3.3 Peculiarities of Time Series Data

3 min

96%

of our students recommend

#1 most reviewed

9 in 10

people walk away career-ready

ACCREDITED certificates

Craft a resume and LinkedIn profile you’re proud of—featuring certificates recognized by leading global

institutions.

Earn CPE-accredited credentials that showcase your dedication, growth, and essential skills—the qualities

employers value most.

Certificates are included with the Self-study learning plan.

How it WORKS

Student REVIEWS